Over the past several years, carbon dioxide removal (CDR) has moved from a niche concept to a market with real volumes, infrastructure, and certification standards covering all CDR pathways. According to CDR.fyi, the durable CDR market now includes around 760 suppliers, more than 1,060 buyers of CDR credits, and nearly 300 marketplaces, registries, and service providers supporting the ecosystem. In total, approximately 46.5 million durable CDR credits have been sold, representing close to USD 12 billion in value.

These numbers show that the CDR market has matured rapidly with strict certification rules, operational systems, and growing supply and buyer interest. Yet despite this progress, the market remains entirely voluntary.

This creates an action gap. According to IPCC assessments, reaching global net-zero CO₂ emissions is not possible without active carbon dioxide removal to balance hard-to-abate residual emissions. Scaling CDR to the levels required by climate science will not happen without a well-structured compliance market that provides long-term certainty, clear demand signals, and room for multiple proven technologies to scale.

For a deeper discussion you can read my earlier article on why net-zero targets alone are not enough.

Why this matters now

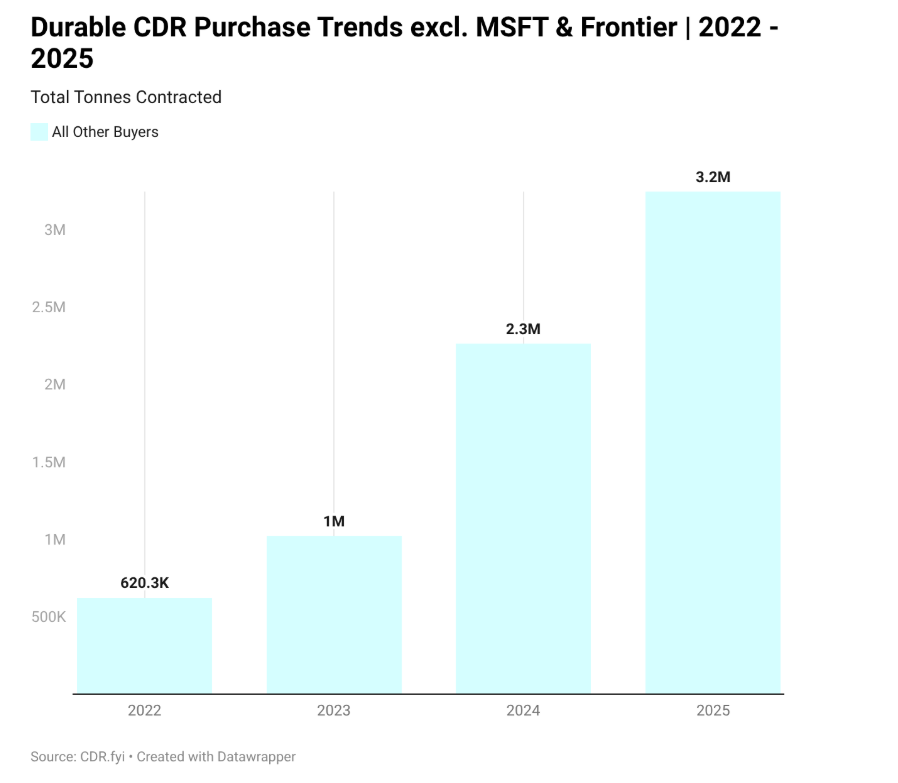

The voluntary CDR market has been shaped by a small group of catalytic buyers. Microsoft alone accounts for roughly 80 percent of all purchased durable CDR volumes, with Frontier contributing around 4 percent. These early movers played a critical role in proving that demand exists and that suppliers can deliver verified removals at scale.

Recently, Microsoft announced a pause in new CDR purchases after contracting around 80 percent of its anticipated needs. This is not a failure of the market. It is a signal that the we need a broader group of corporate buyers.

While purchases excluding Microsoft and Frontier continue to grow year on year, most companies engaging in CDR today do not have any legally binding obligation to remove carbon dioxide from the atmosphere. As a result, some organizations are postponing procurement decisions, scaling back net-zero commitments, or relying on low-quality credits to meet near-term targets. This uncertainty slows down investment, limits financing options, and increases risk for suppliers developing durable CDR solutions.

Compliance demand for CDR is critical for market growth

The CDR industry will not reach its full potential without demand from compliance markets. The integration of carbon dioxide removal into binding policy frameworks alongside emission reduction targets would contribute to:

- Long-term demand certainty: Companies would have a clear reason to secure long-term CDR contracts today that would be used to make a credible claim.

- Improved financing opportunities: Predictable demand enables new financing instruments and increases investors’ confidence.

- Reduced reliance on voluntary action: Business models would no longer depend solely on voluntary commitments.

For durable CDR projects with long operating lifetimes e.g. mineralization of CO₂ in concrete, this certainty is especially important as project partners require confidence that demand will persist.

Technology-neutral approach is essential

While some countries are already actively working on CDR policy, implementation typically takes years. In the meantime, the uncertainty of what technologies will be eligible for crediting under compliance mechanisms creates hesitation among buyers and investors.

A good example is the narrow scope of approved methodologies under the EU Carbon Removal Certification Framework (CRCF). When only a limited set of methods is recognized as “credible” or “accepted,” capital and demand are pushed toward a small subset of solutions, regardless of their scalability or system impact.

This is why a technology-neutral approach is critical. Climate policy should encompass all proven CDR methods that deliver permanent storage and robust monitoring, reporting, and verification. Selecting winners and losers too early risks slowing progress rather than accelerating it.

Integrating CDR into compliance markets requires ambition and structure

There are early signs that policymakers are exploring pathways to integrate CDR into compliance systems, but ambition and structure will determine their impact.

One promising direction is aligning carbon dioxide removal with industrial decarbonisation. For example, the Industrial Acceleration Act aims at strengthening demand for EU-made, low-carbon products through introducing a minimum 5 percent low-carbon requirement for concrete in public procurement. This target could be met by concrete products produced using carbon dioxide curing, which reduce cement content while storing CO₂ permanently. However, modest minimum requirements risk becoming a missed opportunity.

At the EU level, the European Commission is also evaluating whether permanent carbon removal could be integrated into the EU Emissions Trading System. The current focus on CRCF-certified projects, however, remains limited to only a few approved CDR methods. This risks excluding many proven technologies that are ready to scale.

Experts are also examining whether permanent CDR could be included in the Carbon Border Adjustment Mechanism. While this is unlikely before the mid-2030s, the volumes required by 2035–2040 demand investment decisions today, which is only possible with clear policy direction.

Today, durable CDR is priced significantly higher than allowances in compliance markets such as the EU ETS, where prices typically range between €75 and €100. Over time, this gap is expected to narrow as CDR costs decrease and carbon pricing increases. Well-designed policy can help bridge this transition period rather than waiting for perfect price alignment.

The next phase of CDR

Reaching global net-zero emissions is not possible without carbon dioxide removal. Yet there are still no legally binding targets for producing or procuring removals at the scale required by climate science. Despite this, the durable CDR market has developed at remarkable speed and is ready to graduate from being purely voluntary. How fast it scales next depends on integration with compliance markets and mechanisms. Binding demand, technology-neutral approach, and long-term policy signals can unlock investment, de-risk suppliers, and accelerate deployment across sectors, including the built environment.

At Carbonaide, we see CDR not as a distant solution but as a practical tool that can be deployed at scale to match the urgency of the climate crisis.

About Carbonaide

Carbonaide makes carbon-negative concrete economically viable. With the Carbonaide CO₂ solution, concrete manufacturers can utilise carbon dioxide to improve their products and store carbon permanently.