Geopolitical tensions influence global energy markets, and disruptions often create a clear risk premium for oil and natural gas. The recent escalation in the conflict involving Iran has renewed concerns about global energy security.

Even when tensions do not directly disrupt supply, markets often price in uncertainty, and that can lift oil, gas and shipping costs. For Europe, this matters because cement manufacturing depends heavily on heat, electricity and transport. When energy and logistics costs rise, cement production costs usually rise as well.

Learning from the Russia–Ukraine energy shock

Europe saw this dynamic clearly after Russia attacked Ukraine in 2022. Gas and electricity prices increased rapidly, with wide spillover effects across industrial supply chains. Cement manufacturers were exposed because kilns require large amounts of fuel, grinding relies on electricity and deliveries rely on diesel. The result was a fast increase in production costs and broad inflation in construction materials.

When energy markets later eased, cement prices remained elevated. This suggests that cement pricing is shaped by more than short term energy volatility. Once prices reset higher, they often do not revert fully, especially when other cost drivers remain in place.

Why renewed Middle East tensions matter for cement

The Strait of Hormuz is a critical transit route for crude oil and LNG. Even short interruptions can add a risk premium to global prices. In more severe cases, European gas prices could rise sharply, which then affects electricity generation costs, diesel pricing and shipping rates. Those are core inputs for cement production and delivery in Europe.

How energy shocks translate into cement costs

Cement production is sensitive to energy movements across the full value chain:

- Kilns require significant fuel input.

- Grinding and material handling depend on electricity.

- Logistics and on site deliveries depend on diesel and freight capacity.

When these inputs become more expensive, cement producers typically adjust pricing to reflect higher costs.

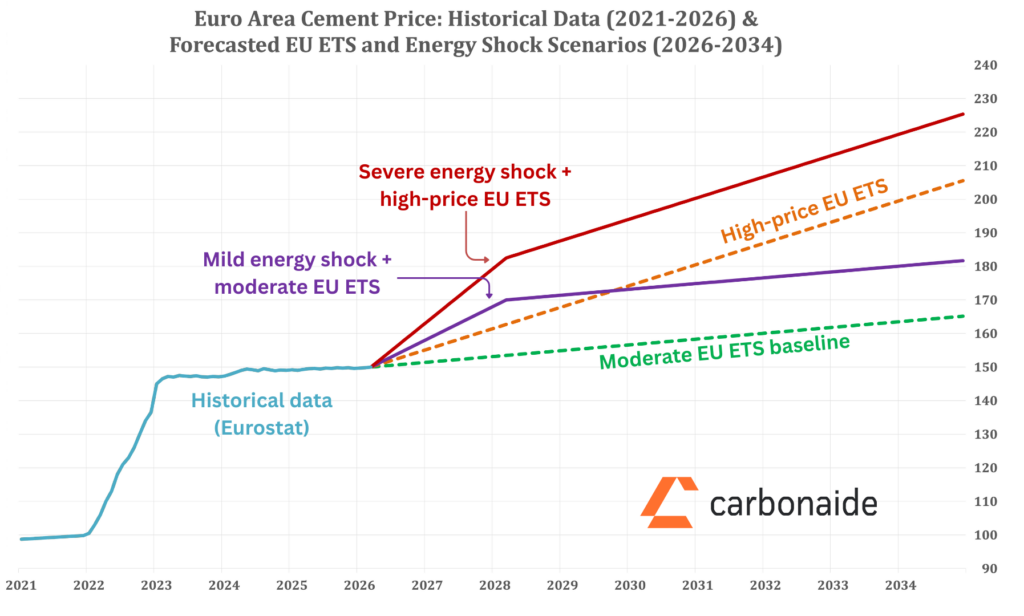

Scenarios for cement price development

Before the latest escalation, European producer prices for cement were already well above pre-2022 levels. In many markets, cement prices have ranged roughly between €120 and €180 per tonne, depending on country, product type and logistics. Using €150 per tonne as a baseline helps illustrate potential outcomes under an energy driven shock.

1. Mild disruption

A short term increase in oil and gas prices raises the energy cost component of cement production by around 30 to 40 percent. Freight and insurance costs add further pressure. In this scenario, European cement prices could rise by €15 to €25 per tonne, lifting averages to around €165 to €175 per tonne.

2. Severe disruption

Extended interruptions in key supply routes keep crude oil above $100 per barrel and European gas prices above €100 per MWh for longer. That strongly affects kiln fuel, electricity and transport. In this scenario, cement prices could increase by €25 to €40 per tonne, reaching roughly €175 to €190 per tonne depending on region. In higher-cost markets, values above €200 per tonne could appear quickly.

Overall, the scenarios imply a price increase of roughly 10 to 27 percent, depending on local starting points and logistics exposure. It can be estimated that such price changes would occur during following two years time period.

Implications for the built environment

Higher cement prices affect budgeting and planning across the built environment. Price adjustments rarely happen instantly because supply contracts can smooth short term volatility. However, sustained pressure in energy, transport and carbon costs tends to feed into market prices over time. Understanding the link between input costs and cement pricing helps builders, designers and industry leaders anticipate shifts and plan procurement accordingly.

Long term cost structures are also shaped by regulation. Cement has been part of the EU Emissions Trading System for many years, and the phase down of free allocation together with CBAM (Carbon Border Adjustment Mechanism) will influence production costs. The impact depends on allowance prices. A moderate scenario may add €10 to €20 per tonne, while higher price scenarios can add €40 to €70 per tonne from EU ETS alone by the end of 2034. In the worst case, all these assumptions can turn out to be conservative.

Other factors also contribute, including raw material costs, inflation, reconstruction demand and geopolitical risk, especially when energy markets are affected. Cement price increases can also extend to supplementary cementitious materials, since availability is limited in Europe and globally. As a result, the economic incentive to reduce clinker content and improve binder efficiency becomes stronger, even while overall material costs trend upward.

How Carbonaide strengthens cost resilience

We at Carbonaide focus on enabling concrete producers to reach the same or improved performance with significantly less cement. Through carbon dioxide curing, CO₂ mineralization and permanent storage in concrete products, our technology supports emission reductions and an improved carbon footprint while delivering stronger mechanical performance.

Our CO₂ curing system, CO₂ flow management and software platform provide a one stop solution that strengthens production resilience by enabling:

- Cement savings

- Improved performance of SCMs

- Increased production capacity

- Permanent storage of carbonates in concrete.

These capabilities help producers reduce exposure to volatile energy markets, rising carbon costs and limited SCM availability. We support the built environment with scalable solutions that are cheaper, faster, stronger and greener, helping manufacturers utilize and store CO₂ while achieving lower emissions in concrete production.

About Carbonaide

Carbonaide makes carbon-negative concrete economically viable. With the Carbonaide CO₂ solution, concrete manufacturers can utilise carbon dioxide to improve their products and store carbon permanently.